How Presidential Elections and Economic Policy Impact Investors

With the presidential election just two and a half months away, economic policy platforms are only now beginning to take shape. This late unveiling has some investors concerned about how each policy platform might impact the economy and financial markets. As with all elections, the perceived stakes are high, and with greater political polarization in recent years, emotions are running as hot as ever. In this challenging environment, what do investors need to know in the months ahead to prevent their political concerns from negatively affecting their financial plans?

The economy is in the spotlight leading up to the election

Political decisions and policies affect our daily lives, influencing everything from our tax bills to industry regulations. This heightens the importance of elections, since they are how we can express our preferences for a range of social and economic policies. However, it’s important for investors to vote at the ballot box and not with their portfolios. History emphasizes the importance of separating our personal views from our investment and financial decisions.

While presidential priorities are important, individual presidents can sometimes receive too much credit or too much blame for economic conditions. Major drivers of long-term economic performance tend to be underlying business cycle trends, which can be far more powerful and long-lasting than any single administration's policies. And, over time, business cycles are what drive investment returns and wealth creation.

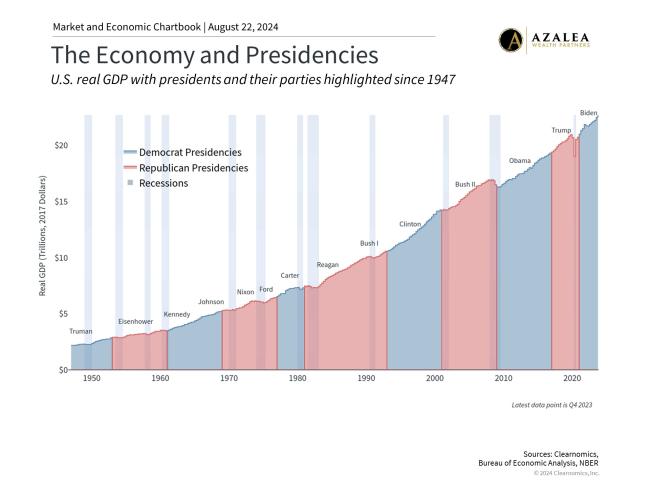

This is highlighted by the above chart, which shows the level of the country’s gross domestic product, a measure of the size of the economy, since World War II. There have been a dozen business cycles and recessions over this period, including the recent pandemic crash, the 2008 global financial crisis, and the 2000 dot-com bust.

These were the result of both external shocks to the economy as well as trends that had little to do with who was in control of the White House. The globalization, information technology revolution, and expansion of financial markets that took place over these years played significant roles as well. The overall pattern is clear: the economy has grown steadily over the past eight decades across both political parties.

Consumers are the central focus this election season

As the candidates’ policy platforms continue to unfold, understanding this context is important. This is not to say that economic policies do not matter, just that investors should be cautious about overreacting to the results of any individual election or a specific policy.

In fact, the economy can impact elections as much as elections influence the economy. This is especially true for this particular election. According to a recent poll by The Economist/YouGov, 24% of Americans rank “inflation/prices” as the most important issue to them, followed by “jobs and the economy” at 13%. This is not surprising given recent market and economic swings due to inflation, interest rates, and Fed policy.

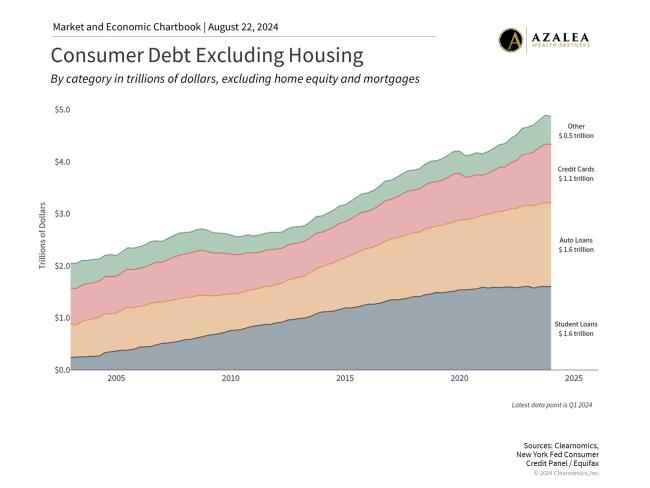

Even though inflation pressures have eased and the economy is showing some signs of strength, very few consumers feel confident in the economy or their financial situations. This is largely because consumer debt has risen dramatically, as shown in the chart above. Total non-mortgage consumer debt has more than doubled in the last twenty years. Credit card debt is at record levels, while student loan and auto loan balances are increasing at their fastest rates since 2003. From the cost of groceries and prescription medications to housing, many American consumers are feeling left behind after the last few years.

Taxes and the deficit are also in focus

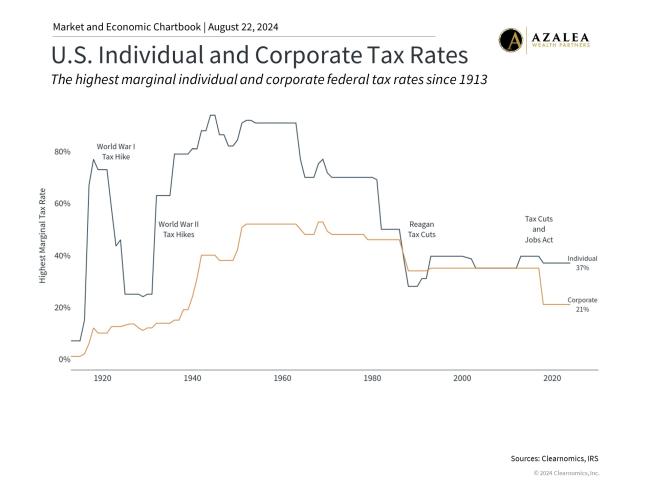

Personal and corporate taxation is also in focus this election. Many policies often stay in place during transitions of power, and the changes that do occur tend to be incremental. In many ways, this is a feature of our political system since it takes broad support to enact new policies, even when the president’s party also controls Congress. For instance, the Reagan-era tax cuts have remained largely intact for decades. Similarly, many of the Trump administration’s tariffs, which were controversial at the time, have remained in place under the current administration.

Of course, tax cuts and credits need to be paid for somehow, either through lower spending in other parts of the federal budget, greater tax receipts, or rising debt levels. These receipts can either occur through higher tax rates in the future or through faster economic growth. Unfortunately, since government spending tends to only rise, recent history shows that the likely result will be higher government debt. Higher tax rates are also a concern among many investors, especially because individual tax rates are still quite low by historical standards. This emphasizes the importance of proper tax planning as investors look toward retirement.

The bottom line? While many investors are nervous about the impact of the presidential election on the economy and markets, history shows that presidents can often receive too much credit or too much blame for long-term economic outcomes. Investors should vote at the ballot box and exercise caution before voting with their portfolios in the coming months.

Copyright (c) 2024 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.